COMMENT: Martin,

After several years of reading your blog, I have concluded that Socrates’ prognostications appear to be spot on. I also share your assertion that a study of history supplies an insight into future events due to the constancy of “human nature.” Where we appear to part ways is in the definition of “money.”

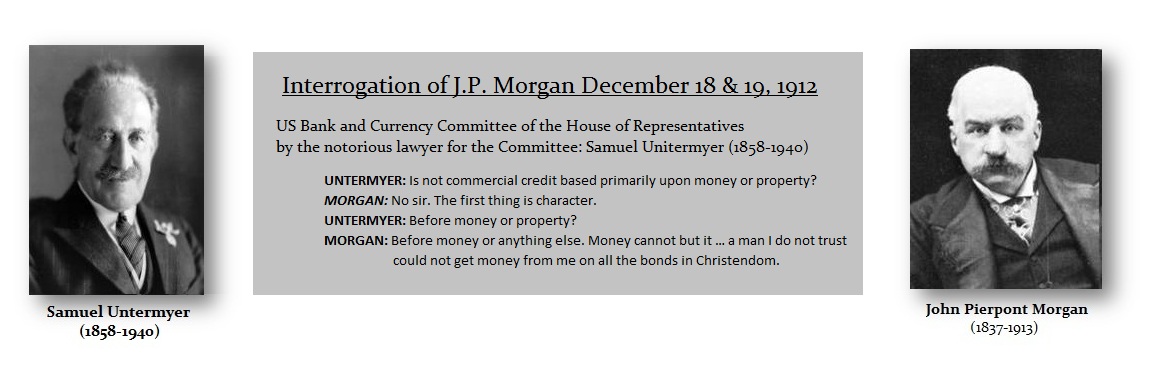

In the early 20th century J. P. Morgan said: “Gold is money; everything else [used as currency] is credit.” Hence, paper money, (and digital entries in an electronic ledger) when issued by a monopolist i.e. government, inevitably descends to its intrinsic value: zero.

AN

ANSWER: Human society has recorded our monetary history and you should not confuse irresponsible government with what is really money. I have a great deal of Respect for J.P. Morgan. If you asked the question of what is money in of a Babylonian, it would be a silver shekel. Even the Bible spoke of weighing the silver and how Judas sold out Christ for a handful of silver coins. To a Greek from Anatolya (Turkey), he would have said it is a stater. To an Athenian, he would say money was a drachma. A Roman would have replied a denarius. But when Rome was first forming, money had been cattle which became thereafter bronze. Indeed, if you had asked before all of them, a Minoan would have said it was bronze. Money has been many things including sea shells in China, and cattle in Europe and Africa.

ANSWER: Human society has recorded our monetary history and you should not confuse irresponsible government with what is really money. I have a great deal of Respect for J.P. Morgan. If you asked the question of what is money in of a Babylonian, it would be a silver shekel. Even the Bible spoke of weighing the silver and how Judas sold out Christ for a handful of silver coins. To a Greek from Anatolya (Turkey), he would have said it is a stater. To an Athenian, he would say money was a drachma. A Roman would have replied a denarius. But when Rome was first forming, money had been cattle which became thereafter bronze. Indeed, if you had asked before all of them, a Minoan would have said it was bronze. Money has been many things including sea shells in China, and cattle in Europe and Africa.

A Spanish during the 15th century would have said it was a one-ounce silver reale. The German would have said no – it’s the silver thaler. The British would disagree and said it was a pound of sterling (.925 silver). The Americans, not wanting to be subservient to England, adopted the dollar, which was a version of the German thaler. In Asia, it was the cash, then the yen.

A Spanish during the 15th century would have said it was a one-ounce silver reale. The German would have said no – it’s the silver thaler. The British would disagree and said it was a pound of sterling (.925 silver). The Americans, not wanting to be subservient to England, adopted the dollar, which was a version of the German thaler. In Asia, it was the cash, then the yen.

Saint Patrick in the 5th Century AD upon his arrival in Ireland, found that MONEY was expressed in human slave girls. He wrote in his Confession, “I think that I have given away to them no less than the price of fifteen humans.” This passage shows something very important. First, MONEY is not defined as the Medium of Exchange exclusively. It also serves the purpose of a Unit of Account. In fact, this becomes the true function of MONEY even more so than what it is. MONEY is a language of value.

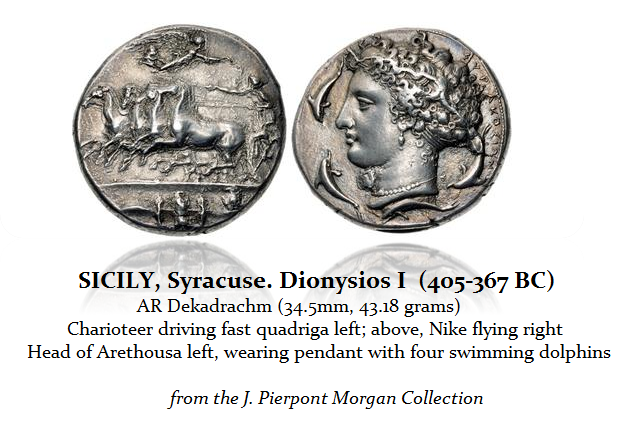

Many of the major bankers, kings, and heads of companies were ancient coin collectors including President Teddy Roosevelt. JP Morgan understood banking and credit – but not money. This was a Syracuse Dekadrachm of Dionysios I (405-367BC) was one of the coins from his collection that was eventually sold by the coin firm Stacks of New York in September 1983. You can download that catalog. People like Josiah K. Lilly Jr. and Paul A. Straub donated their collections to the Smithsonian.

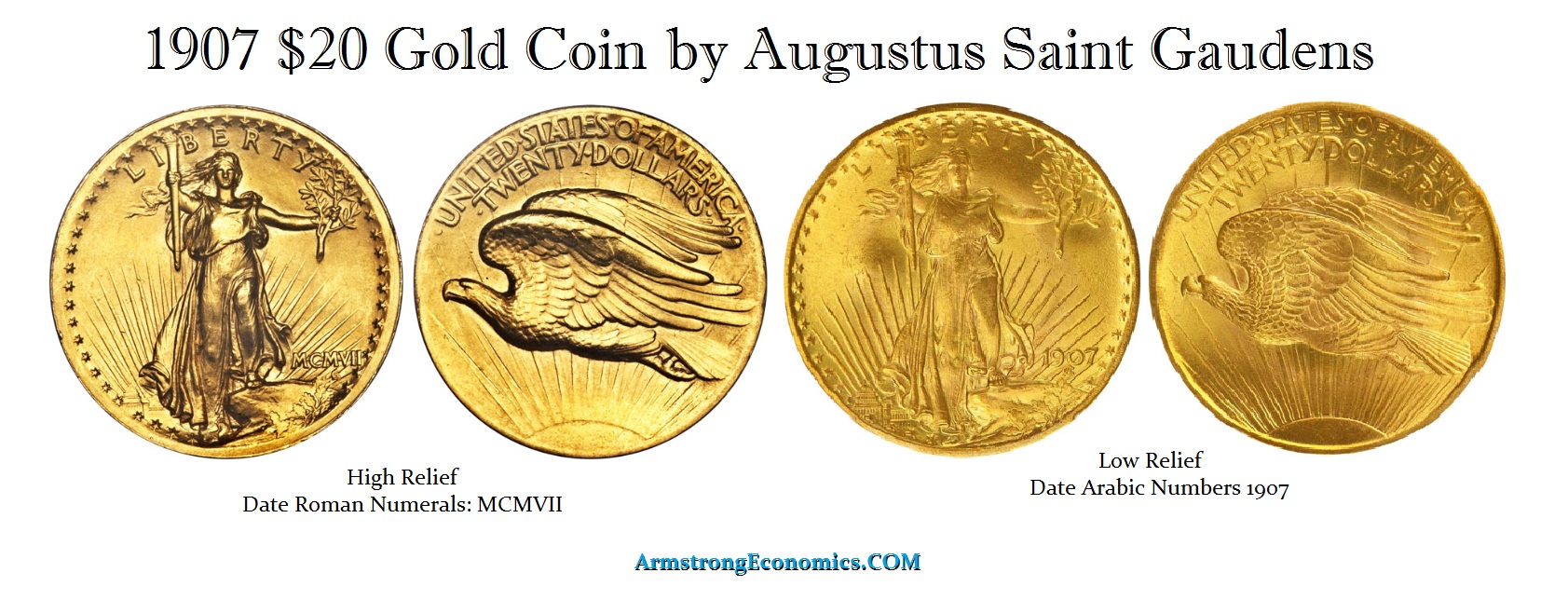

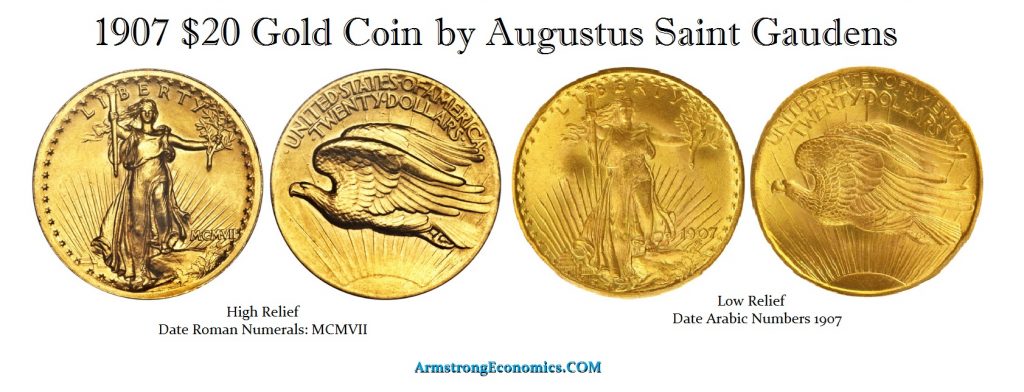

Teddy Roosevelt (1858-1919) loved the high relief of ancient Greek coins. When Teddy Roosevelt became president on September 14th, 1901 – March 4th, 1909, he commissioned the artist Augustus Saint-Gaudens (1848 –1907) to redesign the $20 gold coin and made it high relief as the ancient coins had been struck. The machines could not handle the high relief for the dies would break and they lacked the power of an individual stamping out coins. Thus, the new $20 gold coins had to be reduced in their relief. Nevertheless, we have ancient coins to thank for the limitation on the confiscation of gold in 1934. It was that very reason that his cousin FDR exempted ancient gold coins from confiscation when FDR was himself a stamp collector instead.

Teddy Roosevelt (1858-1919) loved the high relief of ancient Greek coins. When Teddy Roosevelt became president on September 14th, 1901 – March 4th, 1909, he commissioned the artist Augustus Saint-Gaudens (1848 –1907) to redesign the $20 gold coin and made it high relief as the ancient coins had been struck. The machines could not handle the high relief for the dies would break and they lacked the power of an individual stamping out coins. Thus, the new $20 gold coins had to be reduced in their relief. Nevertheless, we have ancient coins to thank for the limitation on the confiscation of gold in 1934. It was that very reason that his cousin FDR exempted ancient gold coins from confiscation when FDR was himself a stamp collector instead.

I would say the problem here is the definition of money and what predates coinage was the development of a weight standard to enable trade. That invention of weighing technology appears to emerge around 3100 to 3000 BC. This was the most significant turning point in monetary history for it marked the beginning of economic history itself.

It was private merchants during the Bronze Age that created the weight systems. Trade took place through informal networks, but it was clearly Mesopotamian merchants who established a standardized system of weights that later spread across the Western region and into Europe. This innovation enabled international trade across the continent. By the second millennium BC, merchants could potentially trade anywhere in Western Eurasia simply by knowing the conversion factors of a multitude of local weight units. What was emerging was the formation of weight systems that was the foundation for the booming commercial interaction of the Bronze Age world.

From the very beginning, MONEY has been a commodity – nothing more. It simply began a barter. I will give you these carrots for potatoes. When the Lydian King Kroisos (561-546BC) created the first bi-metal monetary system, a gold stater was about 10.71 grams and the silver-gold ratio was 13.33:1 because gold was common in Turkey. The inflation caused by the war led to a gold weight reduction to 8.71 grams. Fiscal mismanagement existed from the very beginning. This would have been no different than FDR revaluing gold in 1934 from $20.67 to $35 per ounce.

There were competing standards from the very beginning. The Lydian/ Milesian standard began with an electrum stater at 14.2 grams. The stater as minted under the Euboic Standard was 17.2 grams of electrum. There was the Phokaic Standard placing the electrum stater at 16.1 grams. Obviously, foreign exchange dealers became necessary for international trade among the city-states.

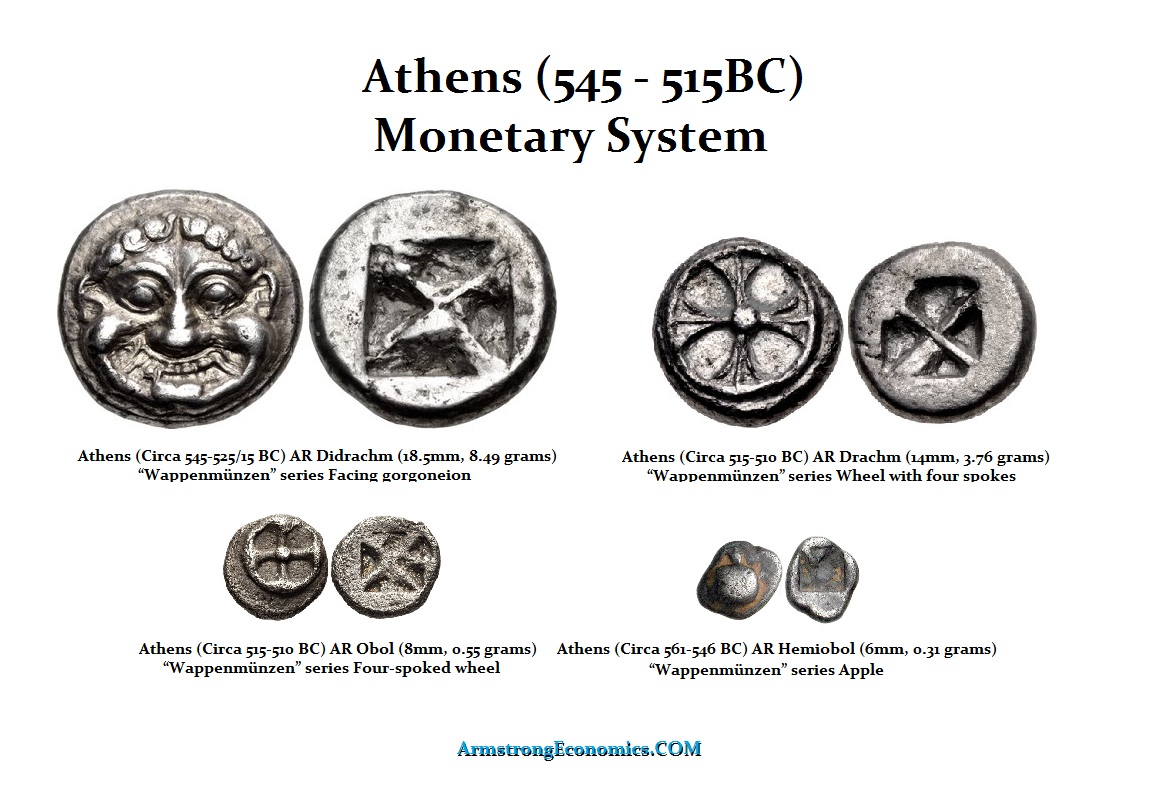

I can find no evidence of a single standard that dominates the nations at this time. By 530BC, the invention of coins spreads to Greece and now the first city-state begins to strike a silver stater at 12.6 grams – the Isle of Aigina. In Greece, silver was common and gold was rare.

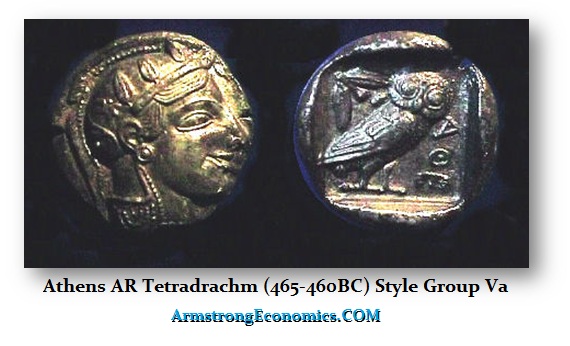

In Athens, they established the Attic Standard based on a silver didrachm (2 drachms) of 8.6 grams, but as inflation emerged, the standard coin became the tetradrachms (4 drachms) at 17.2 grams. So you can see there may have been gold and silver used as MONEY, but by no means was there a unified standard agreement as to weight. In Corinth, they set their stater at 8.5 grams and divided it into three drachms. Standardization comes only with conquest as was the case with Napoleon.

Athens dominated many city-states and in 449BC issued its famous enigmatic “Coinage Decree” promulgated by Perikles that restricted other city-states from striking coins making their coins a single currency. Perhaps it was just a power play. On the other hand, it was most likely just the profit earned over the raw metal cost known as seigniorage. In other words, the coins once minted purchased more in goods than the raw metal.

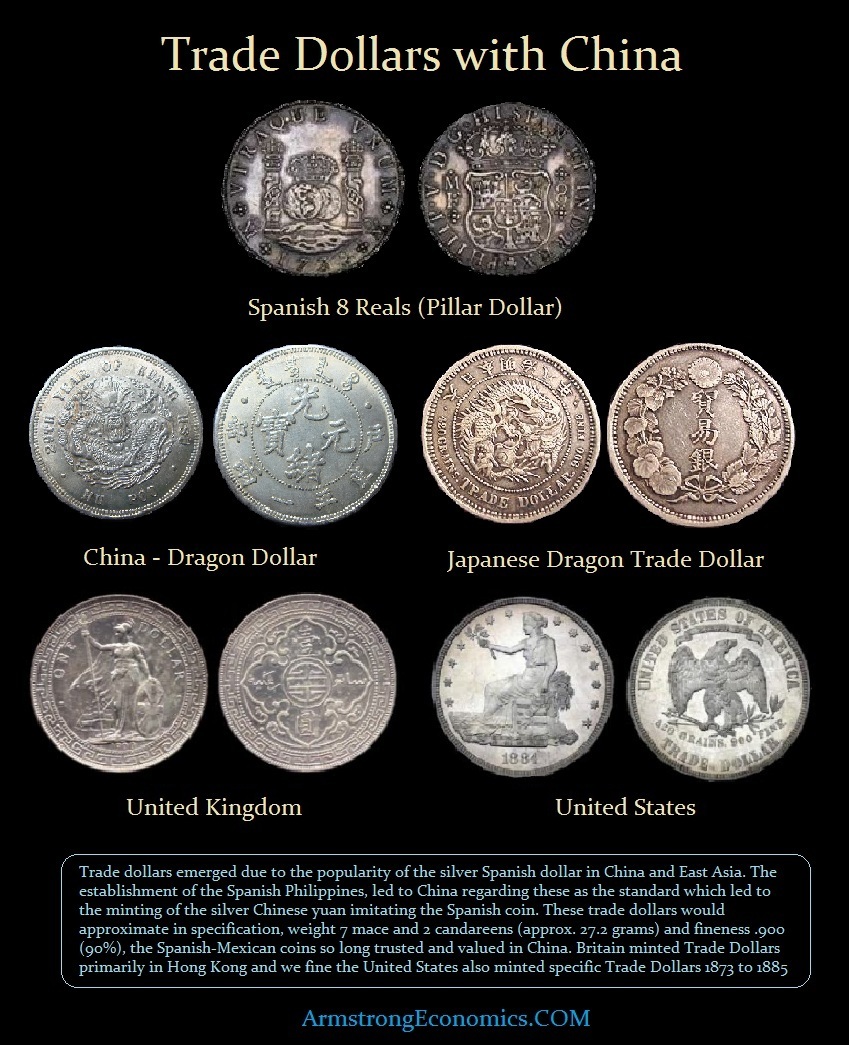

China did not use gold. They had a silver standard. The West had to create silver trade dollars set to their weight standard, which was heavier than the standard United States silver dollar. There have been different monetary systems throughout world history. They have not all been based on precious metals. What it always boils down to is the capacity of the people to produce. There are plenty of places with natural resources and the countries are barely even 3rd world. China, German, and Japan rose from the ashes without gold. Their people produced and they rose to the top of the list of economies despite others having gold.

The bottom line has always been that the wealth of a nation is nothing more than the total productivity of its people. Monetary standards have changed throughout the centuries. What is actually money depends entirely upon what others are willing to accept in exchange. Gold and silver have no real utility value whereas bronze can be used to make weapons or tools. So there is no absolute definition of money, It has changed many times throughout the centuries.

The post What is Really the Foundation of Money? first appeared on Armstrong Economics.